Many of you have read one or both of my books titled: Get Me to ZERO or Tax-Free Millionaire.

Parts of both books describe using select Index Universal Life policies (IULs) for supplemental tax-free retirement income. I call them ROTH alternatives on steroids.

I love ROTHs but they cannot supply nearly the benefits of a properly designed and funded IUL.

A portion of those books also describe what I call “Catapult” plans. These plans combine 5 premium payments from my client (minimum premiums of about $22,000/year depending on age) along with bank financing the rest of the premiums in their IUL (about 65% of the total funding).

For the last dozen or so years, our firm has handled some $4 BILLION of premium loans for these plans for 1,000s of our clients.

What’s very unique for my clients is that there are no loan applications, no credit checks, no collateral (other than the policy itself) nor any personal guarantees. You don’t even sign a loan document! Although 2 years of one’s latest tax returns are required.

Folks must be age 21-60 and in average health as well as have a very good income or asset level.

I realize that many people reading this BLOG POST don’t fit that description. But the comment I get most frequently is that “I wish I knew about this 10 years ago.”

Well, if it’s too late for you to turbocharge your tax-free retirement income, what about letting your successful adult children in on this?

These plans could be retirement gamechangers for your loved ones, too.

I was in Dallas at the annual Kai-Zen (Catapult) conference last week when they announced this easy to use software to compare one’s age, sex, and potential premium (for only 5 years) and see what the estimate of the tax-free retirement income might be.

I encourage you to CLICK HERE to explore the income estimator and learn more for yourself and/or forward this email to your children or folks that you care about.

Your name and email are NOT requested, so you are completely anonymous.

Our proven strategy will provide more tax-free income (and death benefit protection too) than a ROTH (which has ridiculous and outdated IRS mandated income and contribution limits).

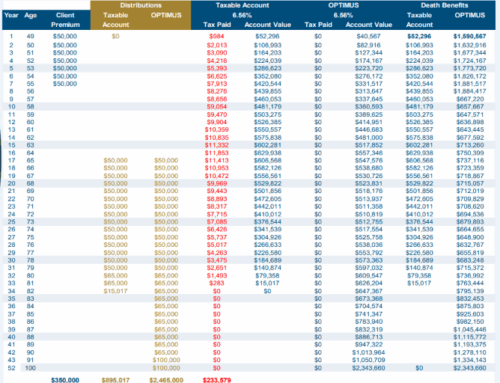

For example. I put in a 50-year-old male with a $40,000 contribution for just 5 years in the plan ($200,000 total from client). The initial death benefit starts out at about $975,000 (and rises over time). But this strategy is built

for tax-free income – not a death benefit.

The bank will loan about $568,000 over 10 years. The bank loan and accrued interest are paid off around year 15 from the policy cash value without any taxation.

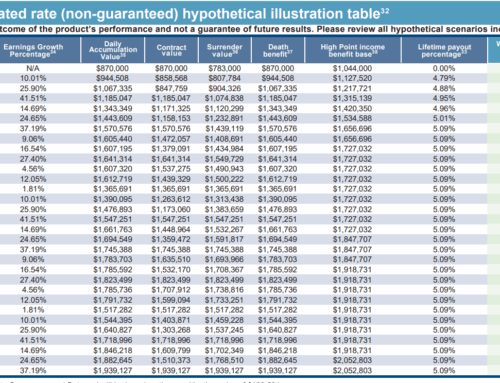

At a 6% average crediting rate, the estimated tax-free income from age 66-90 will be approx. $51,000 per year (totaling $1,275,000 at that point). Assuming he passes away at age 90, the remaining death benefit of roughly $773,000 will go tax-free to his loved ones.

That’s a total tax-free benefit of $2,048,000 (conservatively) on just $200,000 of the client’s committed dollars. That’s OPM (Other People’s Money) in action. We finance our mortgage, why not a TAX-FREE

retirement?

My 40-year-old daughter has one! I’m too old for Kai-Zen, but I do own 6 IULs without bank financing for my own tax-free retirement.

Enjoy the information and the estimator, and of course, reach out to me with any questions. And with all of this market volatility, you’ll be please to know that this strategy has no stock market risk!

all the best… Mark